Richard White devotes a chapter of his new book on

Reconstruction and the Gilded Age, The

Republic for Which It Stands, to declining standards of living during the

Gilded Age.

White writes that

“By the most basic

standards—life span, infant death rate and bodily stature, which reflected childhood

health and nutrition—American life grew worse over the course of the nineteenth

century. Although economists have insisted that real wages were rising during

most of the Gilded Age, a people who celebrated their progress were, fact, going

backwards—growing shorter and dying earlier—until the 1890s.” (page 475)

“The average life

expectancy of a white man dropped from the 1790s until the last decade of the nineteenth

century. A slight uptick at midcentury proved fleeting, nor was it certain that

the smaller rise in 1890 would be permanent.” “What this added up to was that

an average white ten-year-old American boy in 1880, born at the beginning of

the Gilded Age and living through it, could expect to die at age forty-eight.

His height would be 5 feet, 5 inches. He would be shorter and have a briefer

life than his Revolutionary forebears.” “Infant mortality worsened in many

cities after 1880.” (page 479)

White also notes the difficulty of creating historical

statistics but suggests that

“When these

statistics all point in a similar direction, they are worth of some attention.”

In general, White bases his interpretation on excellent work

done by economic historians. I do, however, want to argue that there is less consensus

than he seems to suggest. In other words, the statistics do not all point in a similar

direction when it comes to the Gilded Age.

I also want to point out there is a miscalculation in the statement

about height. White relies on Costa (2015) for the evidence on height; he includes

a version of the graph from Costa (see below) in which one can see that the

series hits its lowest point in 1890 at 169.1 cm, which translates to 5 feet

six and a half inches. I am sure that I would make many more grievous errors in

a 940 page book, but I had already seen the number repeated once as if it were

fact.

Nevertheless, the overall picture that White presents of material

well being during the Gilded Age is consistent with picture in the graph. Clearly

the most noteworthy feature of the graph is the decrease in average height and

life expectancy during the nineteenth century. The average height and life

expectancy fell relative to colonial ancestors before beginning to rise again

in the late nineteenth century. The timing of the movements in the series seem

to be consistent with each other.

Source: Costa, Dora L. "Health and

the Economy in the United States from 1750 to the Present." Journal

of economic literature 53, no. 3 (2015): 503-70.

I want to argue that the evidence of declining living

standards in the Gilded Age is not as consistent as White suggests. Estimating life expectancy in

the United States during the nineteenth century is extremely difficult and different

approaches have produced different estimates. They all suggest that life

expectancy fell during the nineteenth century, but they do not all estimate

that life expectancy reached its lowest point in the late, as opposed to the

mid, nineteenth century. Estimating average

heights is also difficult, and recent work suggests that the series reproduced

by White may overestimate the extent of the decline and place the low point too

late in the nineteenth century.

The United States did not have a death

registry for the entire country until 1933. Some states and localities

registered deaths, but we are left with questions about how representative they

are. One innovative approach to the problem has been to use genealogical

records (see Fogel 1986). Beginning in 1850 the Census began to ask

about people that had died in the last year, which can then be used to

calculate life expectancy. On the numerous shortcomings of both types of data

see Hacker (2010).

Source: Hacker 2010

The above figure is from Hacker 2010 and presents four

different series of estimates of life expectancy at age 20. Only the Haines

series based on census data shows in the late nineteenth century. Both the Pope

and Kunze series bottom out in the 1860s.

Source: Hacker 2010

The mortality rates for several large cities also do not

seem consistent with worsening conditions during the Gilded Age. There is a

reduced incidence of large spikes in mortality, though there also isn’t a clear

trend toward declining mortality rates until late in the 19th

century (See Haines 2001).

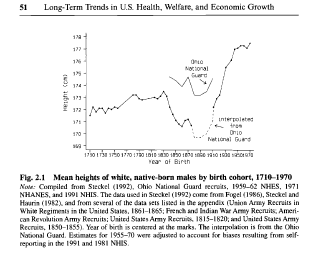

The nineteenth century height estimates are based, for the

most part, upon a large sample of Union Army soldiers. I say for the most part

because late nineteenth century estimates are based upon an extrapolation from

Ohio National Guard data. The figure below from Costa and Steckel shows the

part of the series that is inferred from the Ohio National Guard data.

Source: Costa and Steckel, Long Term Trends in Health,

Welfare, and Economic Growth in the United States

Economic historians have long recognized that there are potential

problems with these estimates. The problem is not just that they might be

biased, but that the bias might change over time. On the other hand, if shorter

than average people became more likely to join the army or the national guard

then our estimates might suggest a decrease in average heights that did not

occur.

Although the potential for selection bias was known, later

research found similar patterns for the antebellum period in a variety of other

populations, for instance Ohio prison inmates (Maloney and Carson 2008) and Pennsylvania

prison inmates (Carson 2008).

Bodenhorn,

Guinane and Mroz (2017) recently argued that sample selection bias is a significant

problem in the height data. Ariell Zimran

has attempted to match soldiers with their census records and use the

information to adjust for selection bias. He concluded that, after adjusting for

selection bias, there was still a decrease in average height of about .64

inches between 1832 and 1860.

Matthias Zehetmayer took a different approach. He developed

a more comprehensive sample of soldiers. Because his observation extended into

the late nineteenth century he did not have to rely on an extrapolation for the

years after the Civil War. The graph below compares Zehetmayers estimates with

previous estimates. His estimates follow the original until you get to

the extrapolation from the Ohio national guard. Zehetmayer finds increases in the 1870s and 1880s rather than a steep decline.

Source:

Zehetmayer 2011

There are a lot of evidence pointing to a decline in height,

but there is no consensus that about when that decline began to reverse or even

if it might be explained by selection bias. Zehetmayer's recent estimates do,

however, seem to be consistent with the life expectancy estimates of Pope,

Kunze, and Hacker, reaching a low point in the 1860s or 1870s rather than 1890.

I think White was right to emphasize the difficulties involved

in creating historical statistics. Like other interpretations of history our

knowledge of material well-being in the past has to be derived from the bits

and pieces that were left behind, even if they are not ideally suited to the

task. Although estimates are very consistent regarding a declining standard of

living in the ante-bellum period, they are much less consistent about a decline

during the Gilded Age. The most recent estimates of both height and life

expectancy seem toward rising standards of living during the late nineteenth

century.